Fintech 2025: The 'New Waves' of Innovation, Security, and User Experience

Alright, "Fintech 2025: New Waves of Innovation, Security, and User Experience." Give me a break. Another breathless article about how tech is going to magically solve all our problems. Seriously, I'm already bracing for the avalanche of self-congratulatory LinkedIn posts.

"Hyper-Personalization" or Hyper-Creepy?

Data-Driven What Now? So, this article is all hot and bothered about "data-driven hyper-personalization." They're acting like fintech companies are suddenly going to become our best friends, anticipating our every need with their fancy algorithms. Right. More like they're going to use every data point they can scrape to squeeze every last penny out of us. They say, "Fintech firms today leverage billions of data points, from spending habits to real-time location, to personalize financial journeys." Translation: They know where you are, what you're buying, and how much you're willing to spend. And they're going to use that information to bombard you with targeted ads and "personalized" offers that you probably don't need and definitely can't afford. I mean, come on. We're supposed to be impressed that AI can now predict when we're going to run out of oat milk? Is that really the pinnacle of human achievement? And let's be real, how much of this "innovation" is just a fancy way to justify charging us more fees? And what about security? Oh yeah, they mention that too. But how much of our personal data is already floating around on the dark web thanks to these "innovative" fintech companies? I'm just saying, maybe focusing on not getting hacked should be a higher priority than predicting my next coffee order."Intuitive" Apps or Just Slicker Traps?

UX: User Experience or User Exploitation? Then there's the whole "user experience" angle. Apparently, fintech companies are now obsessed with making their apps "intuitive" and "seamless." As if slapping a fresh coat of paint on a fundamentally broken system is going to fix anything. Let's be real, the real UX innovation is figuring out new and inventive ways to trick people into signing up for predatory loans and hidden fees. It's like they're designing these things to be deliberately confusing, hoping that people will just click "agree" without reading the fine print. And it's working, offcourse. I miss the days when you could just walk into a bank and talk to a real human being. Now, you're stuck navigating a labyrinth of chatbots and automated menus, all designed to avoid actually helping you solve your problem. And don't even get me started on the "gamification" of investing. Turning the stock market into a video game? What could possibly go wrong? Is this really progress? Or are we just trading one set of problems for another?Fintech's "Regulatory Pressure": Cry Me a River

The Regulatory Minefield Of course, no fintech article would be complete without a nod to the "regulatory pressure" facing the industry. Because apparently, being held accountable for your actions is a burden. It's always the same song and dance: "Innovation is being stifled by outdated regulations!" "We need a more flexible framework to foster growth!" Translation: "We want to do whatever we want without anyone telling us 'no.'" I'm not saying that all regulations are perfect, but let's not pretend that the fintech industry is some innocent victim of bureaucratic overreach. These companies are playing with people's money, and they need to be held to a higher standard. The alternative? Another financial crisis, but this time with even more sophisticated technology to screw us all over. Is This Progress, Or Just a Faster Way to Screw Things Up? I'm not buying it. Fintech 2025: New Waves of Innovation, Security, and User Experience? More like Fintech 2025: Same crap, different year. They want us to believe this is revolutionary, but it's just a new way to exploit people. Then again, maybe I'm just a grumpy old cynic who's afraid of change. But something tells me I'm not the only one who feels this way.

Back to List

Previous Post:Larry Ellison: The Visionary, His Empire of Billions, and Oracle's Game-Changing Next Chapter

No newer articles...

Related Articles

US Government Backs Trilogy Metals (TMQ): Why It's Soaring and What It Signals for America's Future

I just read a press release that, on the surface, is about a mining company in Alaska. And I can’t s...

The Social Security 'Rule' 90% of Americans Break: A Data-Driven Look at the Financial Logic

The financial advisory world operates on a set of elegant, mathematically sound principles. One of i...

Larry Ellison: The Visionary, His Empire of Billions, and Oracle's Game-Changing Next Chapter

The Unseen Threads: How Larry Ellison is Rewriting Our Future, One Safari and Blockbuster at a Time...

Fifth Third Swallows Comerica for $10.9B: Why It's Happening and Why You Should Care

So, another Monday, another multi-billion dollar deal that promises to "create value" and "drive syn...

Spotify's AI Music Initiative: The Strategy, Industry Impact, and What 'Responsible AI' Really Means

Spotify's AI Alliance Isn't About Ethics. It's About Building a Moat. The press releases read like a...

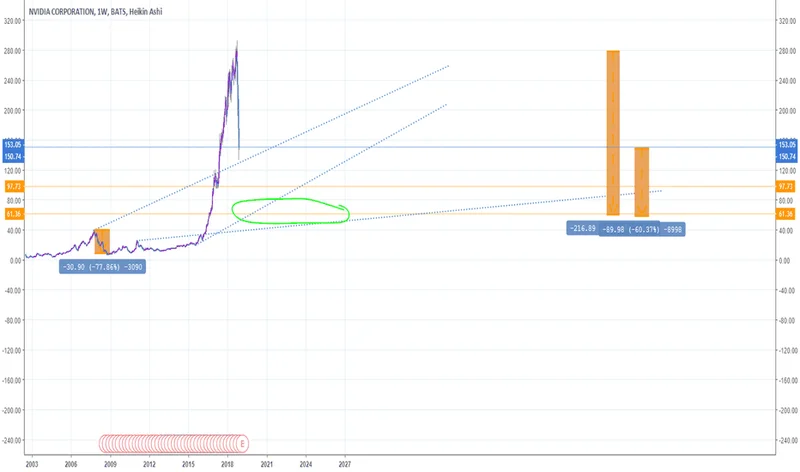

NVDA Stock Is Sinking: Why the Smart Money Is Running and What They're Not Telling You

So, the oracle has spoken. Stanley Druckenmiller, the investing world’s equivalent of a rock god, ha...